WAS THE EURO CRISIS CAUSED BY EXCESSIVE SOVEREIGN DEBT?

By Thomas Fricke

German banks have spent a lot of money and effort to prevent their public image from becoming tarnished since the financial crisis of 2008. But since the euro crisis which started in 2010, the most substantive help for this strategy came free of charge: suddenly, what originally was a banking crisis evolved into a sovereign-debt crisis in the public perception, with the Greeks and others framed as the indebted southerners. Since then, talk shows have not been focusing on issues such as bank-executive bonuses, high-frequency trading or shadow banking, as was the case after the Lehman Brothers crash in 2008, but rather on early Greek pensioners or Italian tax ethics.

No other diagnosis has emerged to become so entrenched and embraced in Germany. It was years of sloppy southern-European government which plunged us into the crisis, so it goes—even worse, the (largely) virtuous German taxpayers have had to pay the clean-up bill.

Obviously, there were southern-European countries getting into trouble. There is, however, a small hitch. Through closer inspection, it becomes apparent that, except for Greece, there is no causal link at all between the outbreak of the crisis and public debt. And this had serious consequences. Regardless of the lack of evidence for the myth of debt as the cause of the crisis, the European Commission, the German government and other guardians of stability tightened the fiscal rules and ratcheted sanctions up against the crisis countries. The EU thus preferred dealing with symptoms rather than with the real cause of the crisis.

A question of sequence

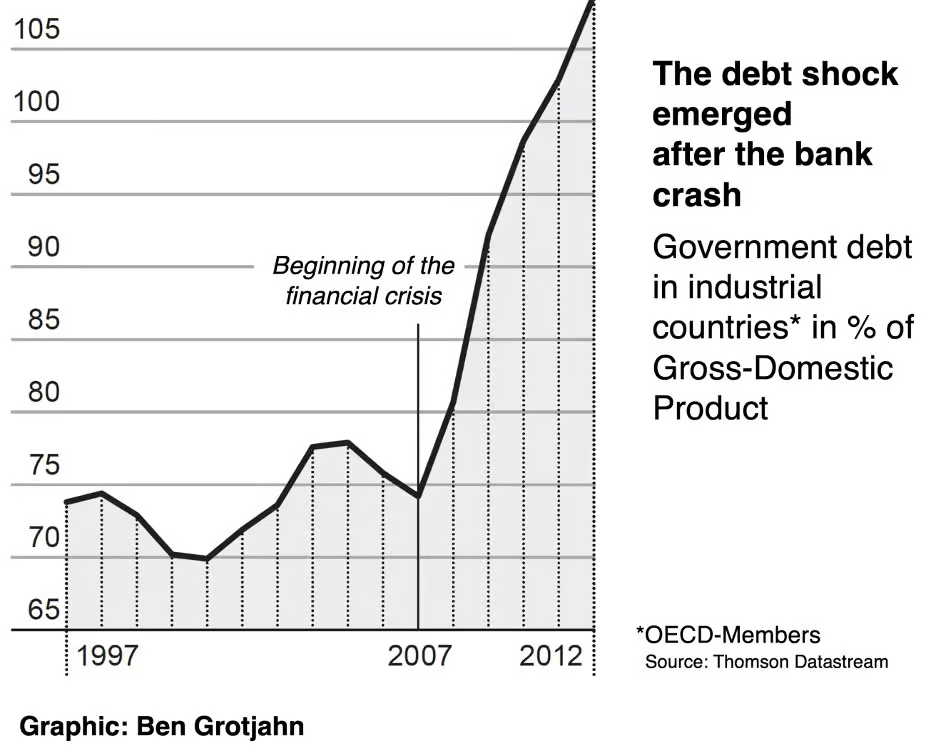

Why were countries like Spain and Ireland sucked into the whirlpool of the crisis? Before the outbreak of the global financial crisis in 2008, both states had budget surpluses. Back then, the accumulated public debt, measured against GDP, was at its historic lowest. Logically, this doesn’t fit into the ‘sovereign debt caused the crisis’ argument. The sequence of events was actually the other way around.

Granted, in the case of Greece, the sequence fits. But why didn’t the markets then start sanctioning the fiscal policy much earlier, through gradually increasing interest rates? Greece’s public finance had been on shaky ground for a while. Why did the credit-rating agencies keep giving Greece A ratings until the end of 2009? This cannot be explained with the usual excuse, according to which the market actors believed the indebted states would be saved in any case, contrary to the no-bailout clause in the Maastricht treaty. Why, then, did the market actors not believe in the same safety net after the crisis?

A more plausible story would be that the markets did not even believe in the possibility of a crisis before its outbreak. Shortly before, international analyses were still reporting that Greece had the second highest GDP growth per capita among all OECD countries since the inception of the eurozone. The OECD’s 2007 Economic Survey: Greece report said on its first page: ‘It is particularly encouraging that growth has been sustained over the last two years, despite substantial fiscal consolidation, mainly being driven by investment and exports.’.

So why did the markets’ opinion change in the fall of 2009? Why had the eurozone member states all of a sudden to pay 5, 10 or 20 percent interest rates, although the 2011 sovereign-debt ratio for the euro area was much lower than in the US or Japan? US and UK sovereign-debt ratios were 40 points higher in 2010 than in 2000; the eurozone only had a 15-point increase. On the other hand, why was Germany spared from rising interest rates—though its sovereign debt shot up by 20 percentage points and remained higher than Spain’s for a while? In 2012, the euro crisis re-escalated despite the drastic austerity packages carried out among the crisis countries. Why did interest rates not decline at this point?

In July 2011, investors even suddenly fled Italy. This happened despite the fact that Italy had already achieved a primary fiscal surplus before interest payments for many years, The same analysts who trusted it before could suddenly recite reasons why Italy was ready to crash, without an ounce of shame.

If the crisis was due to original problems of the crisis countries, it had much more to do with the enormous deficits in trade balances. Numerous countries suffered from increasing deficits, with imports much higher than their exports, while Germany generated ever higher and unsustainable surpluses. Here, at least the sequence is right: first trade imbalances, then the crisis. This is still not enough, however, to explain the peculiar dynamics which led to the escalation of the situation in the eurozone by the summer of 2012. This can only be fully explained in terms of another, deeper phenomenon—the dysfunctionality of the financial markets.

The magic of finance

Either the finance community was wrong beforehand, when rating institutes awarded best grades to the eurozone members and their public finances, or afterwards. It could be both, though, since financial markets are typically known for their erratic switch between euphoria and panic.

Certainly, there existed fundamental reasons to judge countries of the eurozone (or their financial stocks) skeptically. Previous cases, such as the Asian crisis or the boom-bust drama of the ‘new economy’ tech stocks, reflected some basic imbalances of the countries involved. In each case, such skepticism nevertheless quickly developed a life of its own, breeding new problems, and came to plague states which had previously been perceived as solid. This is the so-called domino effect.

Everything that makes up the tricky procyclical logic of financial markets starts from here. Skepticism towards one country may be enough to be wary about the next one. Investors’ flight provides a sign for others to flee as well. Once the downward spiral gains momentum, the usual herd instincts, self-fulfilling prophecies, rating downgrades and speculations within the financial markets suddenly result in crash and collapse. During the euro crisis, doubts about Greece’s fiscal policy—the weakest link in the European chain—suddenly led to investors’ flight and skyrocketing interest rates, which only deepened concerns about the crisis spreading to other countries and prompted more investors to flee. The more investors’ trust in Greek sovereign bonds disappeared, the more restless were the investors holding Portuguese or Irish bonds.

The Nobel prizewinner Joseph Stiglitz said at the time: ‘Had the Greek government bonds’ interest rates initially been kept at 3 or 4 percent, the crisis would not have escalated.’ This could have been achieved if, for instance, the German government had guaranteed the payment of Greek debt early enough. According to the Princeton economist Markus Brunnermeier, the same debt situation can develop in different ways: expected difficulties can exacerbate the fear of a crash, such as when interest rates skyrocket, which triggers panic, or that panic may be soon halted, interest rates stay stable and the situation can be controlled.

Both scenarios are possible outcomes for the markets. The phenomenon is called ‘multiple equilibria’. The first option represented an escalation of the euro crisis, a so-called equilibrium of terrors. The second would have ended in a quick de-escalation, a soft landing. The downward spiral could, and should, have been stopped much sooner to support the second scenario. Who’s at fault?

If the crisis followed the logic of a typical financial panic, the main thing was to counter the malfunctioning of the market as quickly as possible. Then there could not have been any serious doubt about the solvency of a country. In this case, it was a fatal mistake to hold off financial aid to the states requiring it, as the German government did in early 2010. This led to even more panic among already uncertain investors who held southern-European sovereign bonds. It was also counter-productive to link each package of financial aid to conditions and so uncertainty—even more reason for restless investors to dump money. In such a crisis of trust, it was not a good idea to hesitate and chastise Greece with punitive interest rates, which made the servicing of debt only harder. Or to enforce ever further expenditure cuts and higher taxes—believing that it was simply a crisis due to high sovereign debt—which damaged the economy further and resulted in tax income evaporating. It is clear why so many new austerity packages and prime ministers did not help. The chancellor, Angela Merkel, and other European authorities seem to have underestimated the momentum of the financial markets in the face of all public-debt mania, and contributed greatly to the escalation.

The last resort

In such a crisis, only one thing helps, suggested Charles Wyplosz of the University of Geneva—‘a lender of last resort’ which ultimately saves the system. When the loss of confidence turns into panic and people run to banks to collect their money, the system collapses because the banks concerned immediately go bust. At this point it’s already too late. Previous experiences with bank busts have resulted in establishing deposit-guarantee funds.

How little the actual condition of public finances mattered was visible at the moment of the turn for the better. The real assurance came through the July 2012 announcement by Mario Draghi, head of the European Central Bank, that, if necessary, it would intervene massively in the sovereign bond markets—not through a sudden improvement of some public-finance data. Draghi’s quasi-guarantee worked: the announcement itself was enough to save investors from their own fears, hence resulting in Italian and Spanish interest rates returning to normal levels.

It is a lesson that is missing from textbooks on how financial markets (dys)function. Regardless of all home-made problems, the euro crisis was yet another very bitter chapter in the history of the failures of financial capitalism. Sovereign debt increased after the onset of the crisis, not before. Therefore, sovereign debt could not have been the cause of the crisis and it is ironic that the mandated austerity cure increased rather than reduced sovereign debt in various countries.